News & Articles

Rates on the rise: What’s happening with inflation?

In the midst of a so-called Cost of Living Crisis, it can be easy to get overwhelmed by what feels like a constant barrage of headlines about price rises.

References to inflation are seemingly relentless, charting increases in everything from the fuel going into our cars to the food going into our trolleys – all of which has a direct impact on the money in our bank accounts.

So, with inflation hitting 10.1% in July – its highest level for 40 years – here we look at what’s happening and consider what’s likely to happen next.

What is inflation?

Inflation is based on the annual rate of change in the Consumer Prices Index, which itself is based on a basket of over 700 commonly purchased goods and services. This basket encompasses a broad mix of items, including everyday essentials, such as a loaf of bread, as well as one-off luxuries, such as holidays and cars.

In May 2022, the rate of change pushed inflation to 9.1%, moving up from the 9.0% recorded the previous month.

The view from the bank

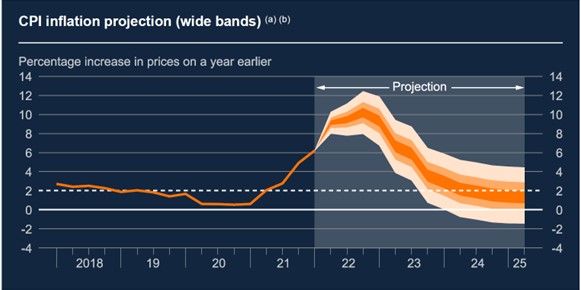

Bank of England, the UK’s central bank, sets the monetary policy that influences inflation, and it has a target from the Government to maintain the rate at 2%. The bank says higher energy bills could lead to inflation reaching as much as 13.3% in autumn 2022 before it starts to slow down next year. In around two years, it expects the level to have fallen back to the 2% target.

The bank presents these forecasts in fan charts to reflect the inherent uncertainty in such predictions, and they are also subject to revision. However, the Governor of the Bank of England, Andrew Bailey, reiterated this projected position to MPs at a parliamentary committee hearing in recent months.

Credit: Bank of England

Credit: Bank of England

What do other projections say?

In its UK Economic Outlook report published in June, consulting firm KPMG suggested that the rate of inflation will average out at 8.1% in 2022, which is marginally higher than the 7.9% it had earlier forecast. KPMG suggests the rate will ease to an average of 4.1% across 2023 before returning to the Bank of England’s 2% target in the second quarter of 2024.

In separate analysis, major City firms were asked for their predictions of inflation in the final quarter of 2022. The average was recorded as 7.8%, and there was also unanimous agreement that the rate would fall notably the following year, averaging out at 2.8% in the final quarter of 2023 – but with some suggesting that the rate could be as low as 1.0%.

What are the major factors influencing inflation?

One of the main contributors to rising costs, and therefore inflation, is the soaring price of wholesale gas and energy. The Economics Observatory highlights how between the summer of 2021 and early spring 2022 forward market prices essentially doubled, with the annual wholesale cost for an average household rising from £528 to £1,077.

The increase in the energy price cap scheduled for October 2022 is expected by many, including the Bank of England, to trigger further upward pressure on inflation towards the end of the year.

The conflict in Ukraine has been an influential factor. While the UK is not reliant on Russian gas supplies, the same cannot be said for the rest of Europe, and the impact of rising wholesale costs on the mainland have been felt in UK energy markets. The war has also disrupted supplies of essential foodstuffs, such as wheat, and with no immediate end in sight, it could continue to exert influence as global markets adjust.

Covid-19 has also played its part in generating inflationary pressures, both in terms of the longer-term legacy from several years of supply-chain disruption and also the influence of more recent lockdowns in China, which have placed continued pressure on the production and distribution of goods.

Further analysis has pointed to the influence of Brexit as a potential catalyst for the UK’s inflationary woes.

What can be done?

The complex range of contributing factors make it difficult to forecast the trajectory of inflation with full certainty. This complexity hints at the fact there is also no single, simple measure for addressing or combating inflation and ensuring rates return to their lower target level.

The most powerful weapon in the Bank of England’s armoury is arguably to increase interest rates, thereby making borrowing more expensive, encouraging saving and reducing spending. It has already implemented this strategy to some extent, pushing interest rates up from a pandemic low of 0.1%, and further rises are expected. We will consider the knock-on effects of increases in the interest rate in a subsequent article.

In summary, with the lever of interest rates at their disposal, the Bank of England is focused on its mission to rein inflation back in over the longer-term. In the shorter term, with energy hikes in autumn predicted to lift inflation to levels not seen since the 1970s, it’s a subject that’s unlikely to descend down the news agenda at any point soon.

The information contained within this communication does not constitute financial advice and is provided for general information purposes only. No warranty, whether express or implied is given in relation to such information. Vintage Wealth Management or any of its associated representatives shall not be liable for any technical, editorial, typographical or other errors or omissions within the content of this communication.

RECENT POSTS

-

Rental health: Assessing opportunities in the buy-to-let market24/06/2025

Rental health: Assessing opportunities in the buy-to-let market24/06/2025 -

Inheritance tax: Incoming changes that could affect your pension20/05/2025

Inheritance tax: Incoming changes that could affect your pension20/05/2025 -

Spring Statement 2025: Summary of key points28/03/2025

Spring Statement 2025: Summary of key points28/03/2025 -

Proceed with caution: Insight into crypto investing26/02/2025

Proceed with caution: Insight into crypto investing26/02/2025 -

Cost of giving: Tax considerations for gifting09/01/2025

Cost of giving: Tax considerations for gifting09/01/2025